BEFORE YOU BUY - CONSIDER THIS

In my 20 years as a mortgage expert, I've been told by buyers:

✅ I'm waiting for the market to crash.

✅ I’m waiting for rates to drop.

✅ I’m looking for a good deal.

In the meantime, everyone who bought:

15 years ago = 2010 was an amazing time to buy

10 years ago = 2015 was an amazing time to buy

5 years ago = 2020 was an amazing time to buy

4 years ago = 2021 was an amazing time to buy

3 years ago = 2022 was an amazing time to buy

2 years ago = 2023 was an amazing time to buy

1 year ago = 2024 was an amazing time to buy

❌ BUT WAIT! What about rates. It’s so much more expensive today! It can't possibly be a good deal to have purchased when rates were so high?!?

Yes, rates went up‼️ And prices stayed the same, and in some cases continued to rise.

Price growth slowed down, but inventory rose, and still it remained a seller's market.

✅ So what does that mean ⁉️

✅ What happens if rates go down now⁉️

✅ I’ll tell you: prices will go up‼️

And they’ll continue to go up.

And when rates do go down savvy investors will refinance.

✅ Lets put this mathematically:

House is $500,000

Rate is 7%

Payment $3,100

👉🏻 Rate drops to 5%

What does price do (in a seller's market)⁉️

✅ It goes up!

👉🏻 Price is now $580,000

Refinance at 5%

Payment now: $2,600

Now, if you bought at $580,000, the rate is 5%, the new payment would be $2,930.

Not a huge savings but now another big chunk to pay off. And guess what⁉️

✅ In 10 years that place will still be north of a million and that loan will be paid down 20% (or more). Another happy buyer.

✅ And if rates never go down, prices still go up!

Why⁉️ Inventory. Growth. And my favorite: inflation.

✅‼️ Inflation is like America’s gift to real estate investor. Loaf of bread goes from $5 to $10. House goes from $500K to $1M. Cha-ching.

Now I was never one to believe in the “date the rate, marry the house” sales pitch, and I especially hated the 2/1 buy down. But i am a believer in good debt + time.

👉🏻 And in my opinion, I would rather owe less debt, and have a higher rate, then have more debt and have a lower rate. One’s eaiser to pay off than the other. Just my 2 cents.

And isn’t it funny; the best times to buy are usually when everyone says it’s the worst⁉️

✅ Like in 2009 when people were losing their houses and there was financial chaos: great time to buy.

✅ Or in 2016 when rates came down and multiple offers were the norm, going 10-20% over asking: great time to buy.

✅ Or in 2020 when covid hit and the market was terrified: great time to buy.

✅ Or in 2021 when rates hit 3% and homes were selling no inspections, cash, 40 offers and six figures over: great time to buy.

✅ How about this: 2006 right before the big crash: great time to buy.

Oh yeah, all the people that “overpaid” now have massive equity in their real estate. Could they have possibly waited a year and paid 20% less, maybe?

But who knows if they would have bought⁉️

Or that they could because of life/financial changes.

I can tell you this, they sure are happy now.

And the truth is, those who are in real estate: aka those actively buying real estate themselves, regularly, are always buying.

✅👉🏻 Because there are always good deals.

✅💪🏻 There is always money to be made, and ultimately all buys are “great deals” in the rear-view mirror.

So be careful who you listen to!

People love talking about real estate…few actively purchase and hold real estate consistently over a long period of time.

🙈 Opinions are everywhere. And opinions and advice are not always fact.

✅‼️ Most people are drowning in information but starving for wisdom‼️

❤️ Find someone who has what you want.

❤️ Who has built their life themselves.

❤️ And go out for coffee.

❤️ Ask them for help.

❤️ They will meet you if you ask.

I guarantee that person will tell you exactly what to do. And I bet it will be hard and contain a great deal of sacrifice and commitment. And it will be worth it.

✅💪🏻👊🏻 Now go find your next deal.

Approved In As Little As

15 Minutes

IT’S EASY WHEN YOU HAVE AN INITIAL APPROVAL

Want to feel good about making a strong offer on your dream home?

Get an initial approval for your loan almost instantly when you work with independent mortgage professionals like us. Our cutting-edge process lets us do what big banks and retail lenders can’t and give you an initial loan approval in as little as 15 minutes — even on the weekends!

You’ll also enjoy greater transparency so you can gather any paperwork you need ahead of time and make sure your loan goes through as smoothly as possible.

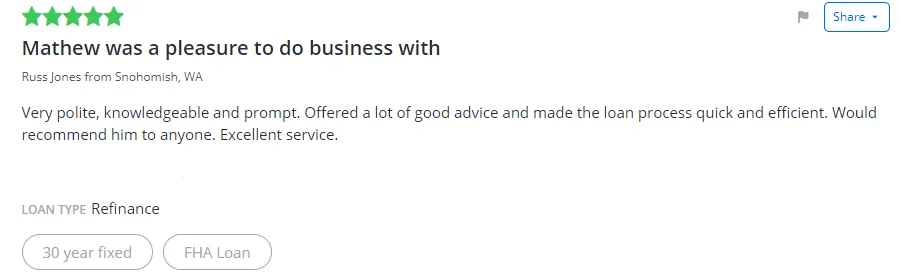

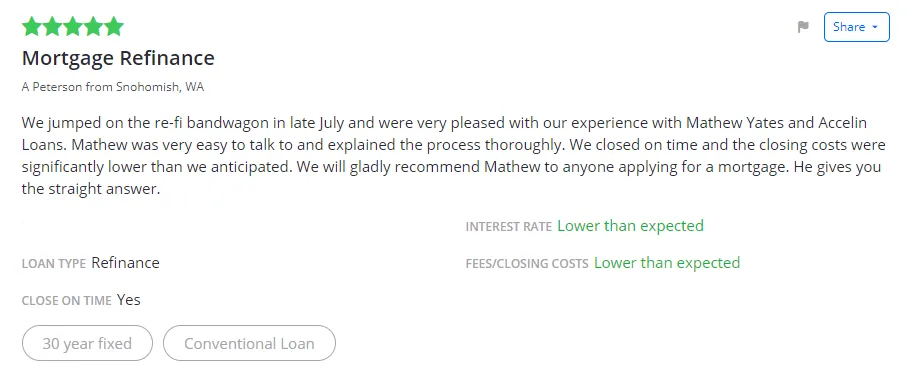

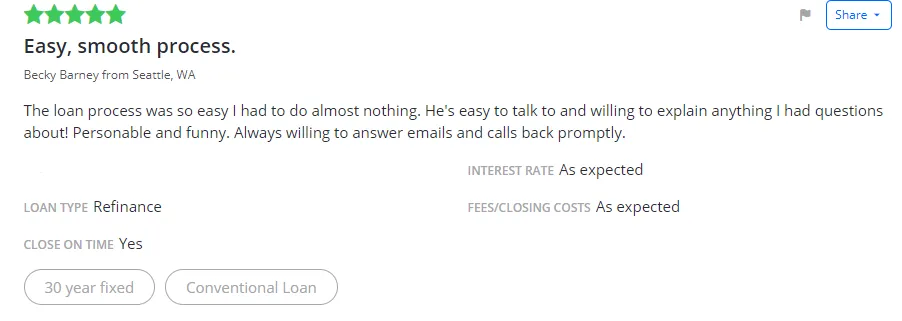

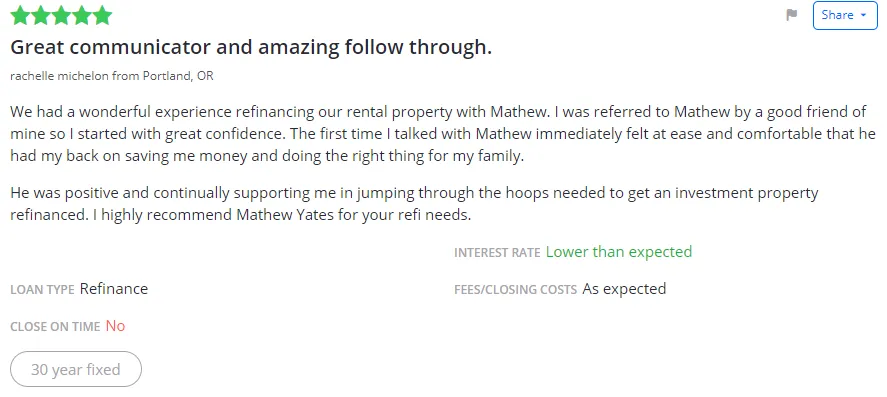

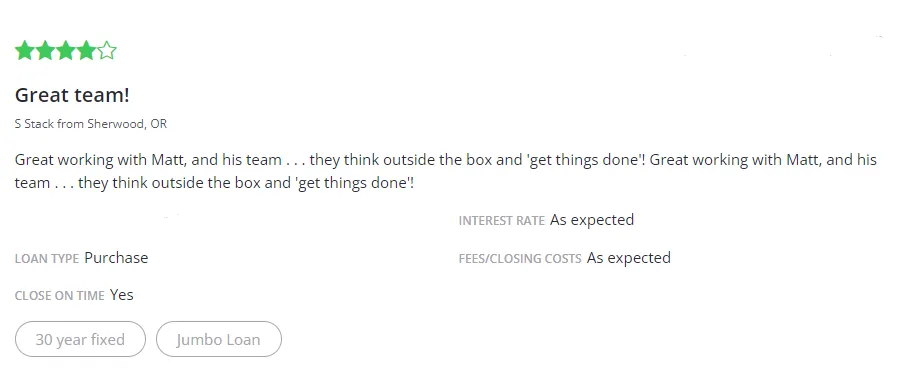

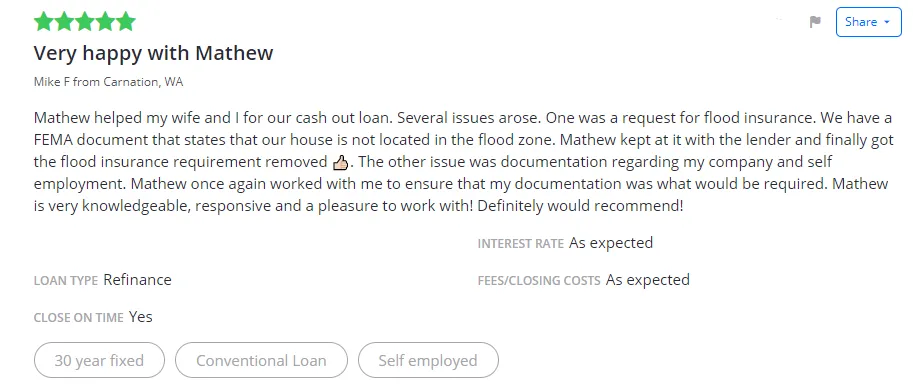

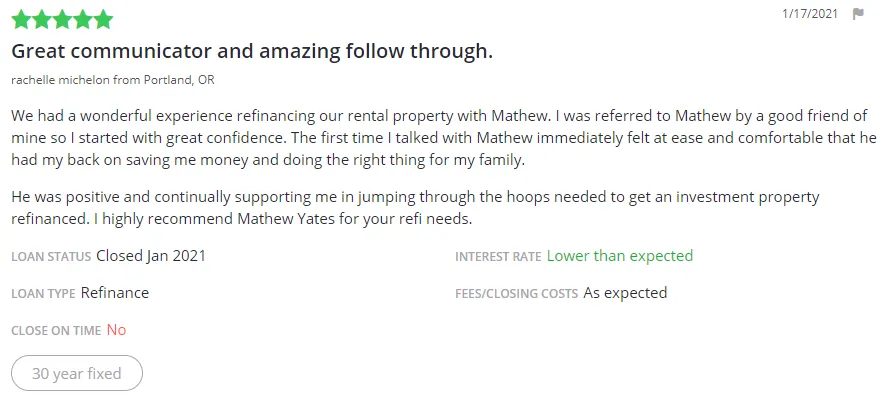

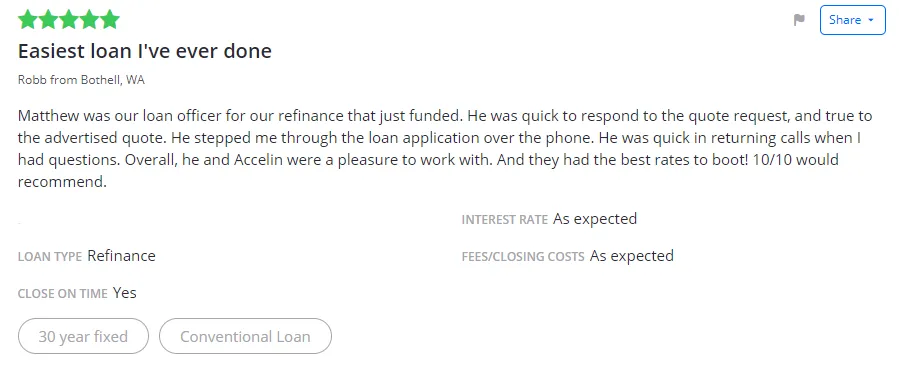

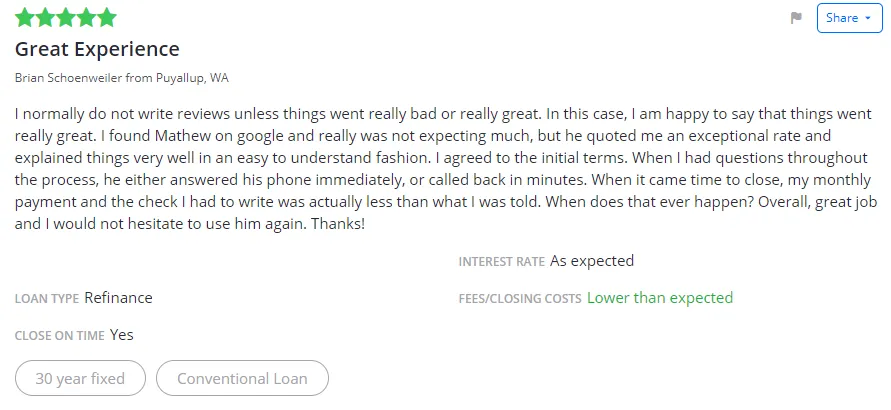

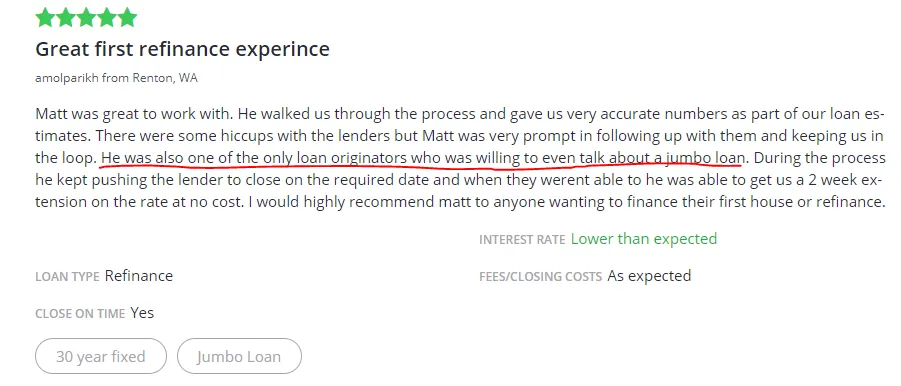

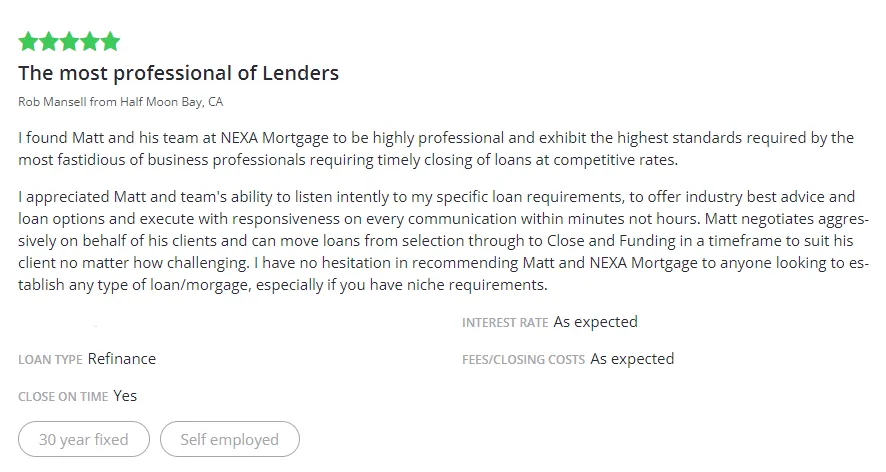

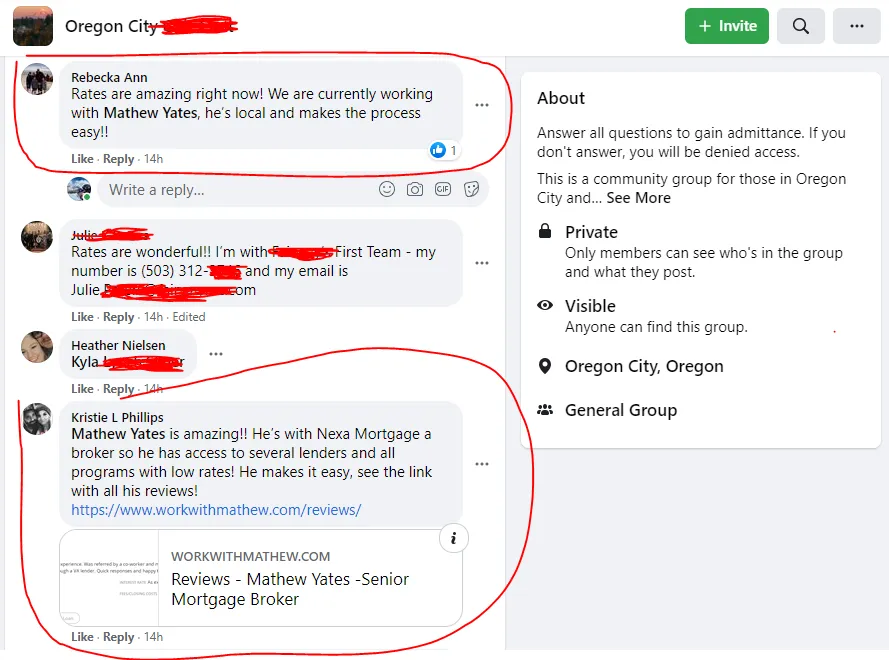

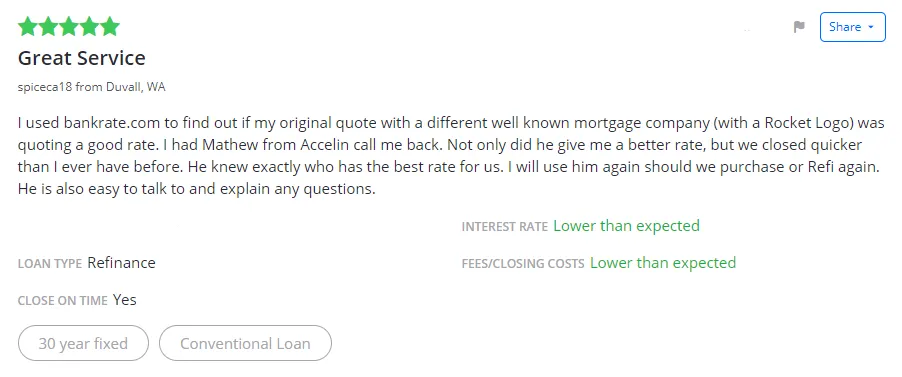

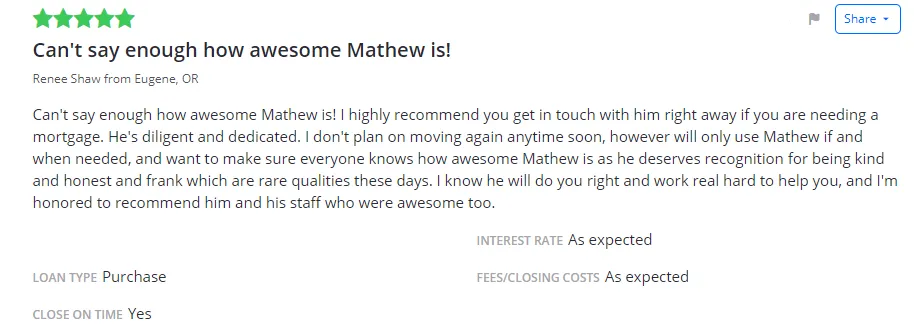

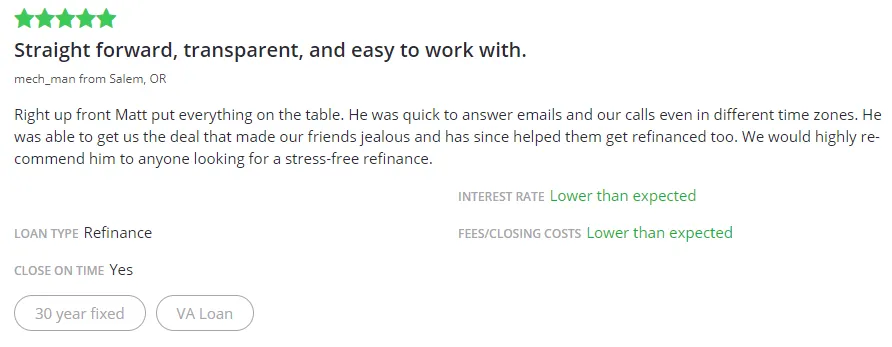

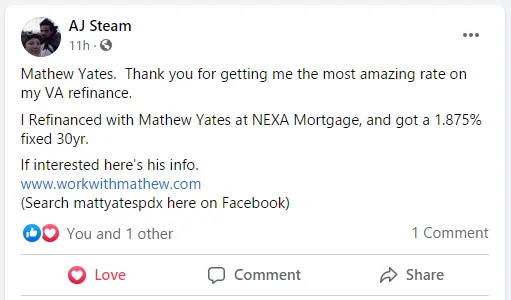

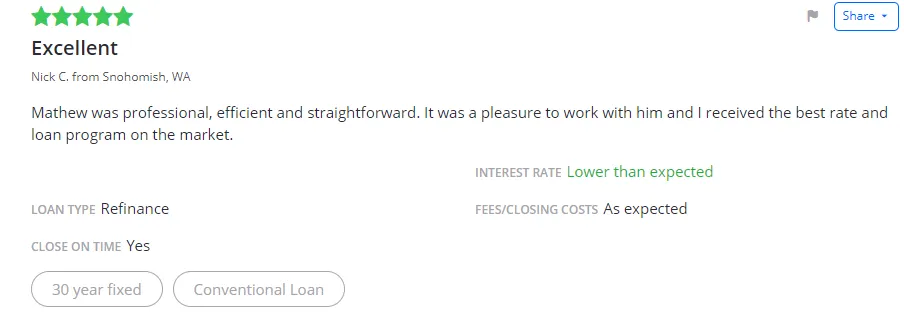

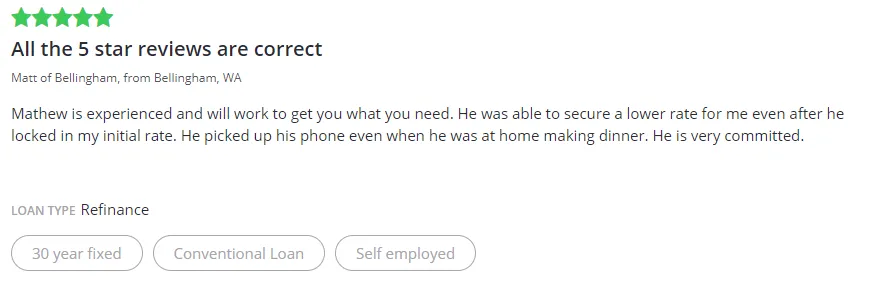

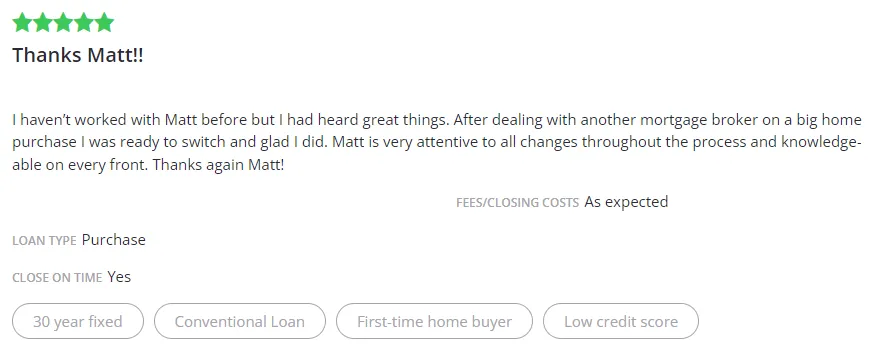

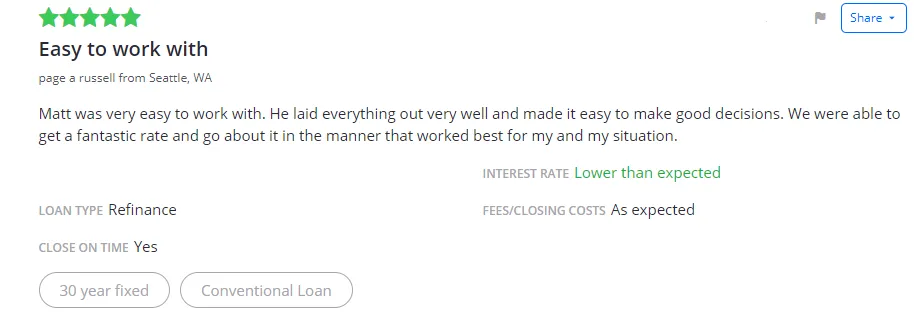

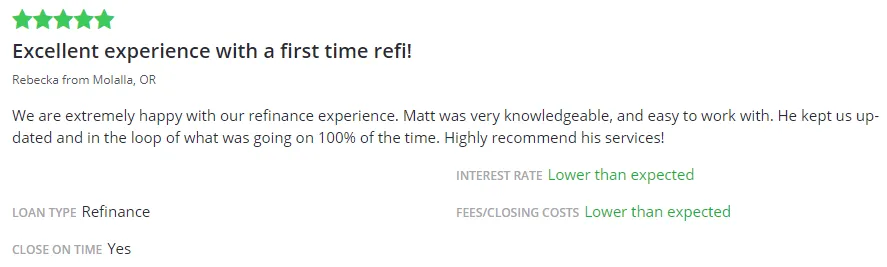

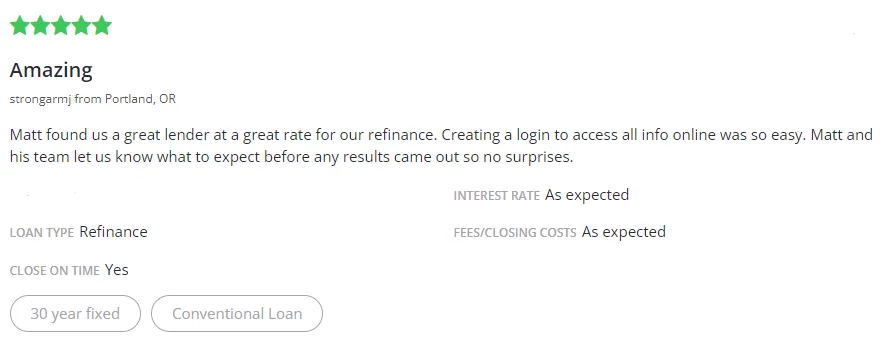

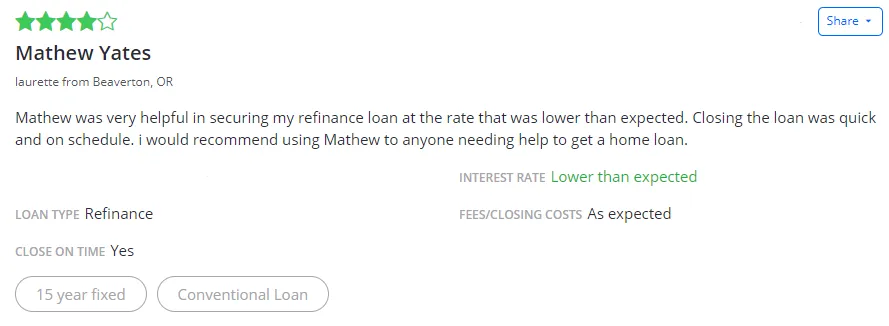

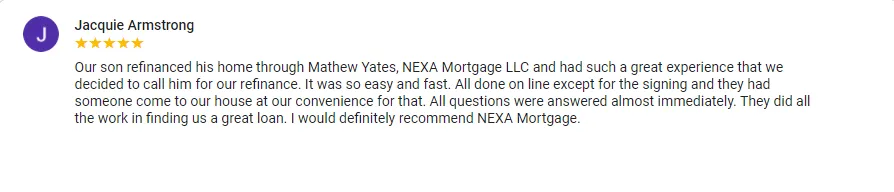

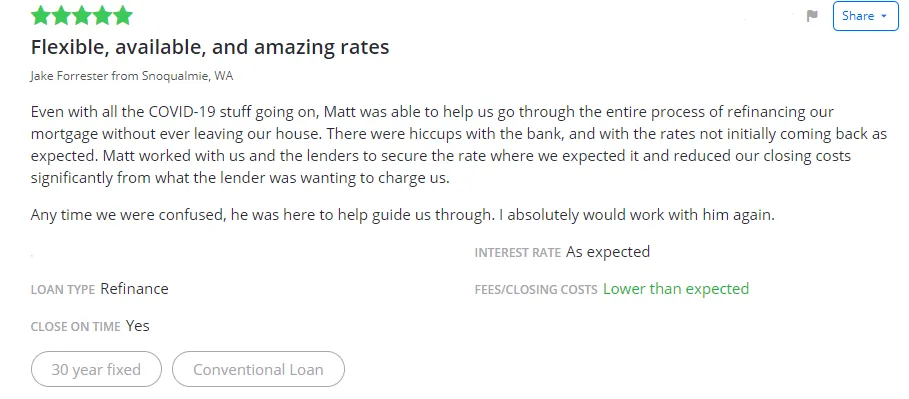

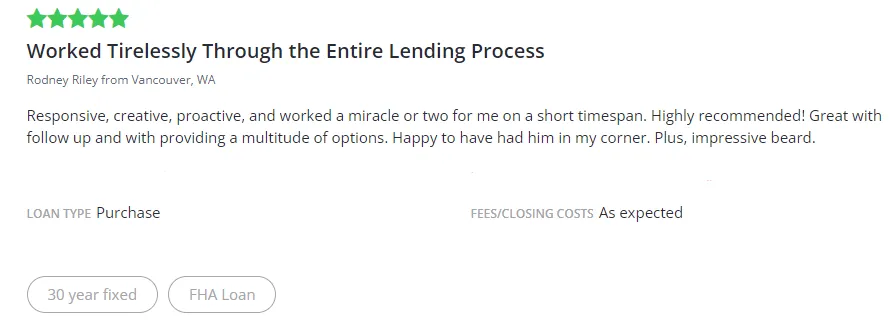

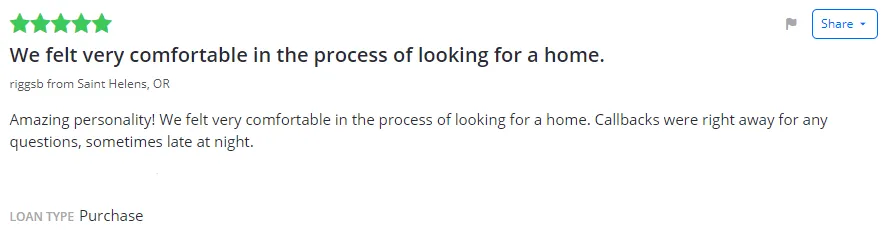

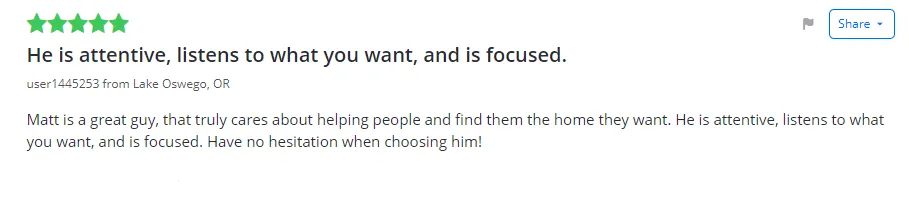

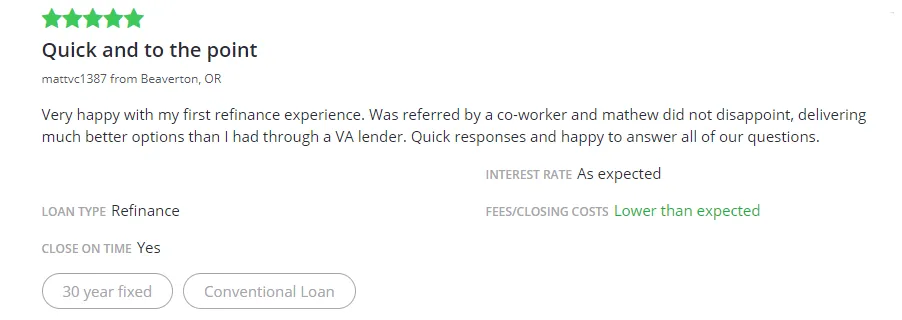

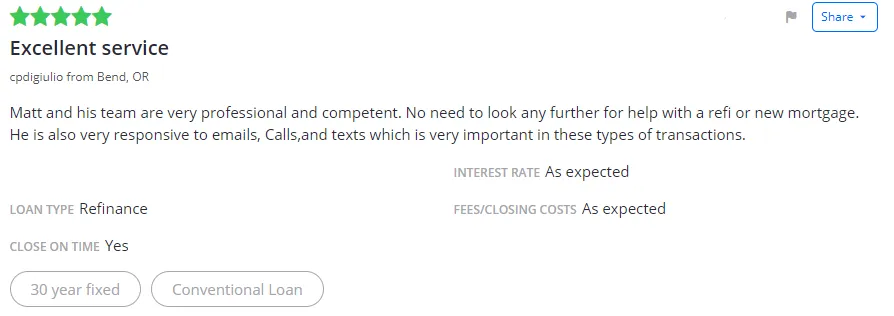

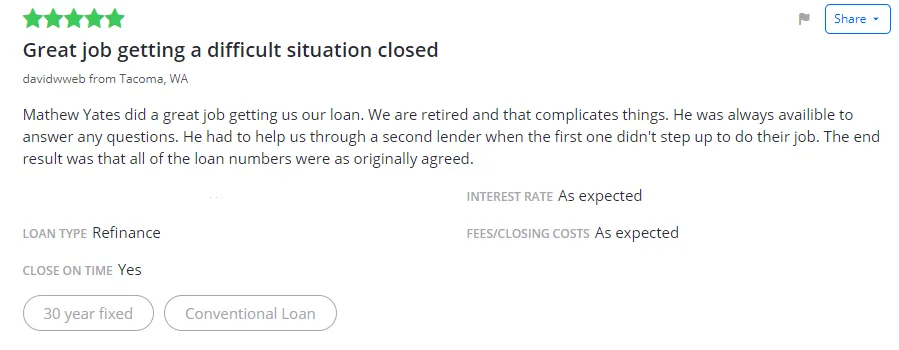

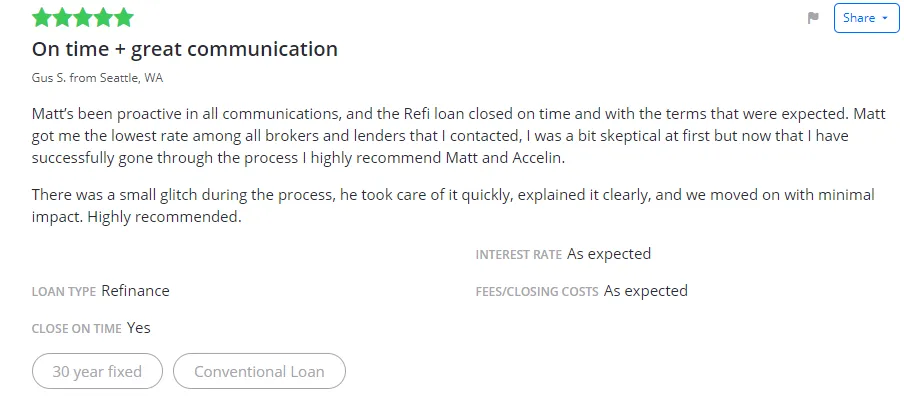

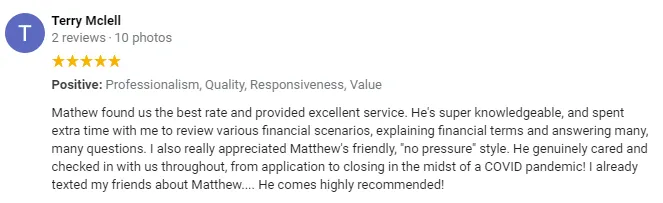

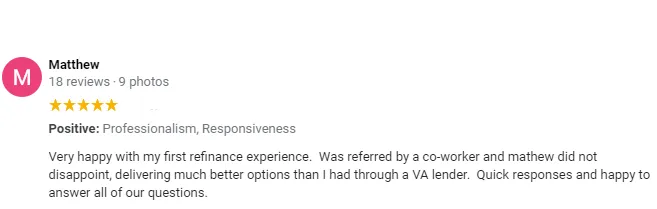

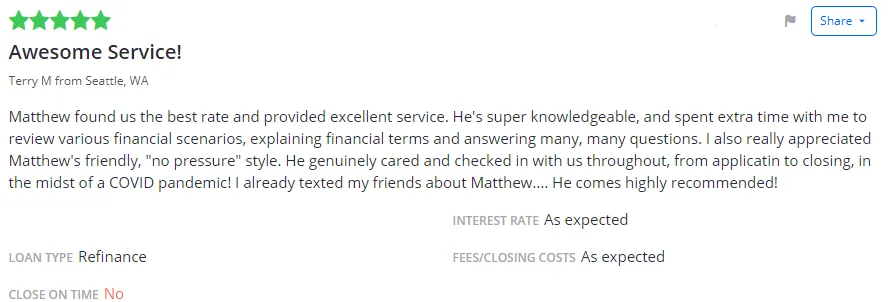

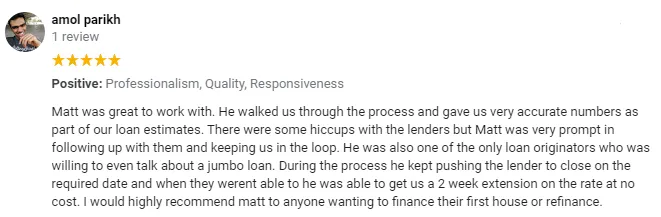

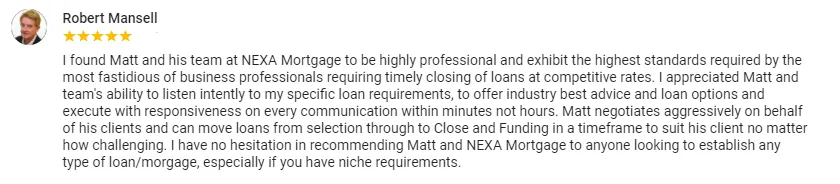

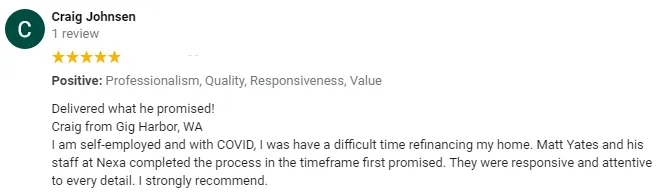

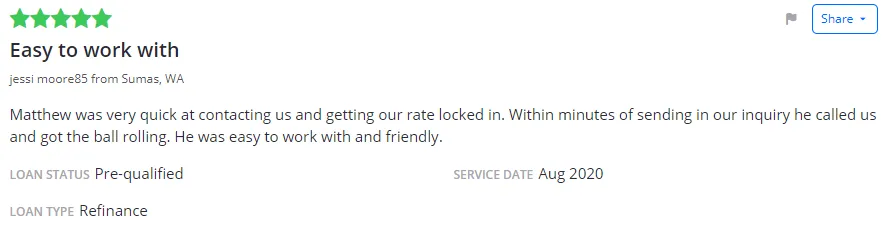

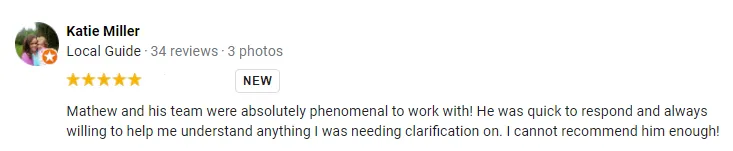

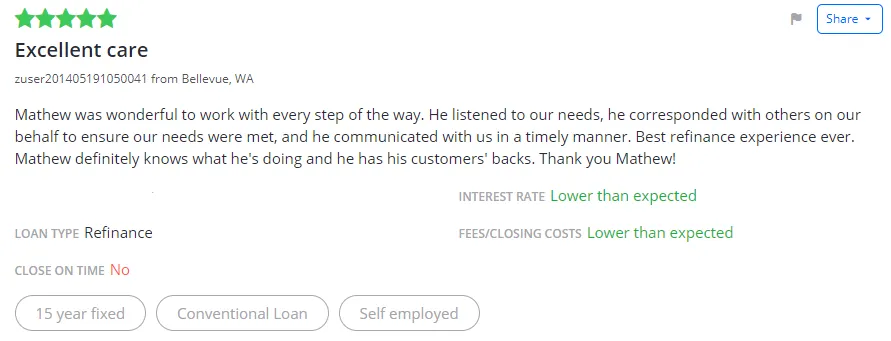

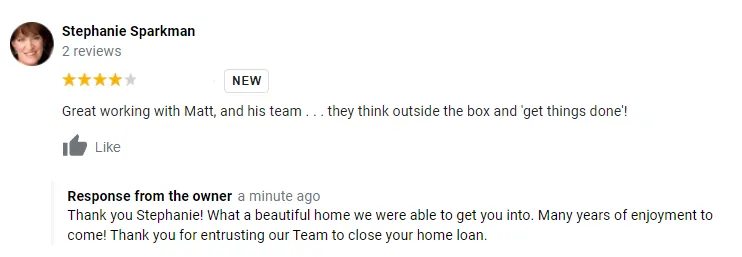

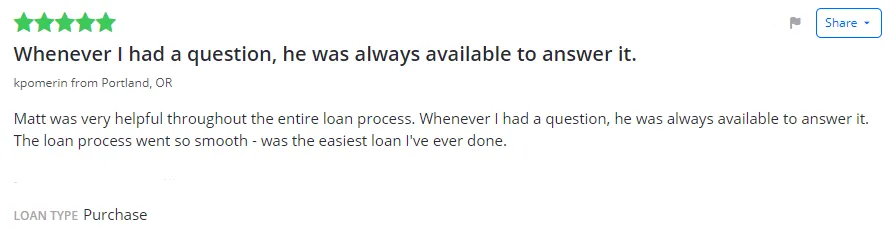

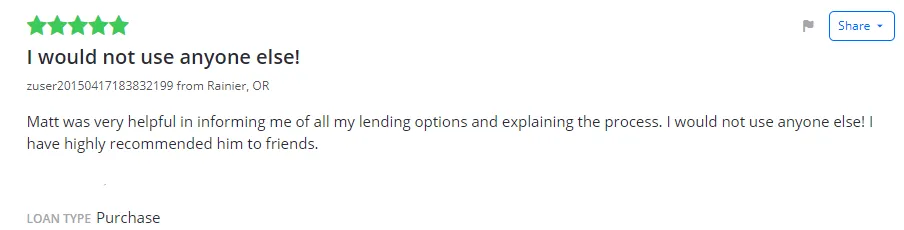

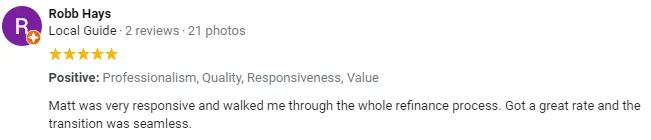

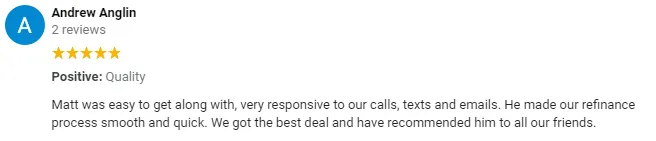

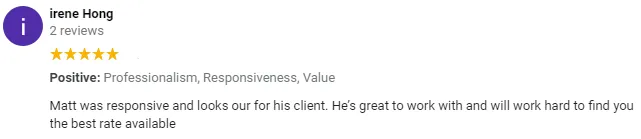

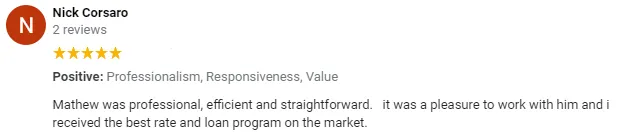

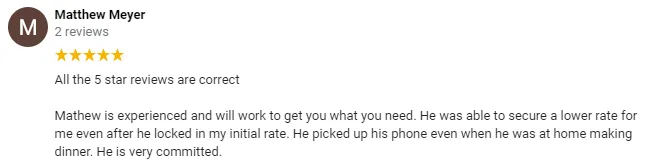

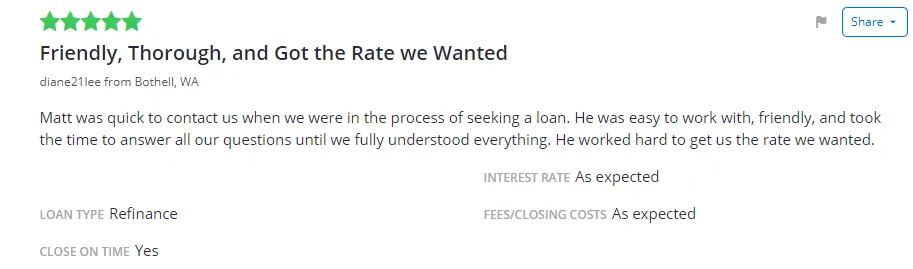

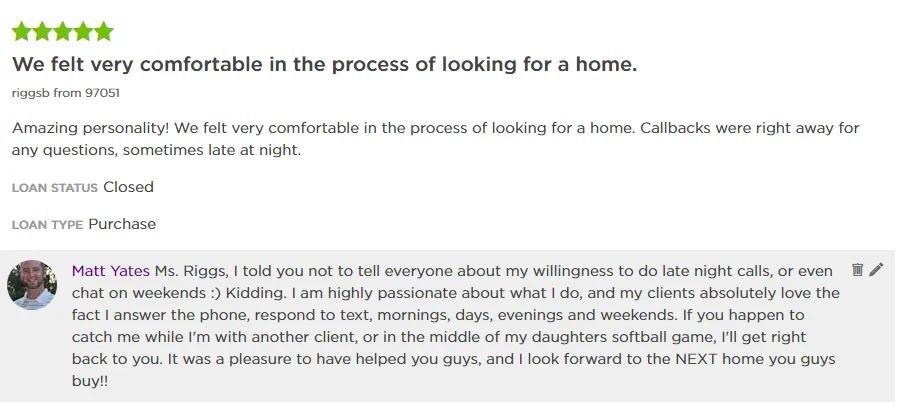

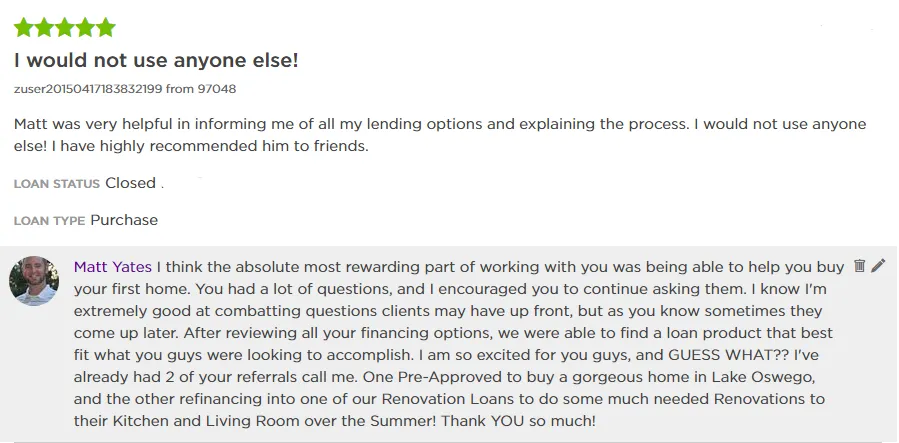

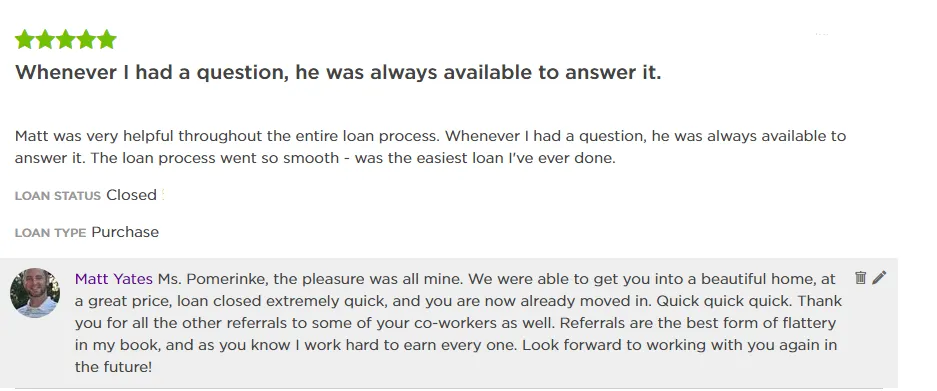

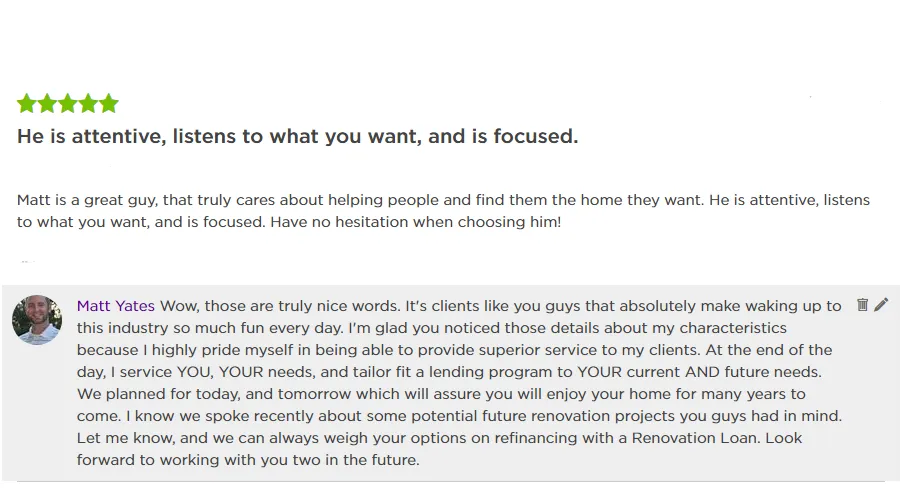

Testimonials

NMLS ID #423065

Contact Me

20225 Water Tower Blvd. Suite 400, Brookfield, WI 53045

NMLS ID #1173903

Novus Home Mortgage, a division of Ixonia Bank is an Equal Housing Lender. We are headquartered at 20225 Water Tower Blvd. Suite 400, Brookfield, WI 53045. Toll free (844) 337-2548. NMLS No. 423065 (www.nmlsconsumeraccess.org). This is not an offer to enter into an agreement or a commitment to lend. All loans are subject to credit approval as well as program requirements and guidelines. Rates and requirements are subject to change without notice. Not all products are available in all states. Other restrictions or limitations may apply. Novus Home Mortgage, a division of Ixonia Bank is not affiliated with any government agency. © Novus Home Mortgage. All Rights Reserved | Program, Rate & APR Examples | Accessibility